What is Section 179?

Essentially, Section 179 of the IRS tax code allows businesses to deduct the full purchase price of qualifying equipment purchased or financed during the tax year. That means that if you buy (or lease) a piece of qualifying equipment, you can deduct the FULL PURCHASE PRICE from your gross income.

It’s an incentive created by the U.S. Government to encourage businesses to buy equipment and invest in themselves. This incentive is for computer equipment, software, and labor placed in service by December 31, 2022.

Section 179 at a Glance for 2022

2022 Deduction Limit = $1,080,000

This deduction is good on new and used equipment, as well as off-the-shelf software. To take the deduction for tax year 2021, the equipment must be financed or purchased and put into service between January 1, 2022 and the end of the day on December 31, 2022.

2022 Spending Cap on equipment purchases = $2,700,000

This is the maximum amount that can be spent on equipment before the Section 179 Deduction available to your company begins to be reduced on a dollar for dollar basis. This spending cap makes Section 179 a true “small business tax incentive” (because larger businesses that spend more than $3,780,000 million on equipment won’t get the deduction.)

Bonus Depreciation: 100% for 2022

Bonus Depreciation is generally taken after the Section 179 Spending Cap is reached. The Bonus Depreciation is available for both new and used equipment.

The above is an overall, “birds-eye” view of the Section 179 Deduction for 2022. For more details on limits and qualifying equipment, as well as Section 179 Qualified Financing, please read this link carefully.

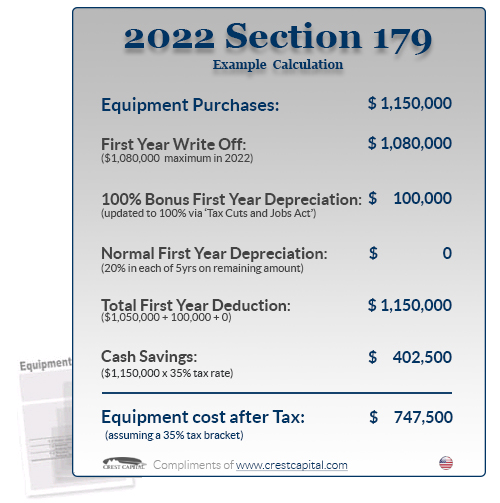

Here is an updated example of Section 179 at work during the 2022 tax year:

Visit http://www.section179.org/ for more information.

*The information contained herein is general information and is not intended as professional advice. The program does not assume you are eligible to take advantage of the IRS Section 179. You should consult a tax advisor or accountant for additional information.

{kind=link}

{kind=link}